Coronavirus (COVID-19) Stimulus Package – What You Need to Know

Toilet paper jokes and mayhem aside, the Coronavirus threat is very real and we’re now seeing an unprecedented impact across the globe.

We woke up this morning to hear that the USA has banned travel from main-land Europe, whilst the Australian F1 has been cancelled, just one day before it was due to start.

These are decisions that are not being taken lightly and will have massive impacts on both macro and micro economic communities. Stock markets around the world have crashed at rates faster than that seen during the GFC.

However, we agree with Scott Morrison when he says that it will pass, and it is more important than ever that we all work together to get through this next phase of this global pandemic.

Putting their money where their mouth is, on 12 March 2020, the Australian Government announced a $17.6 billion economic stimulus package to support individuals, businesses and households affected by the rapidly spreading Coronavirus.

Below we highlight the five main points of the stimulus package and how they might impact you personally, or your business.

1. Cash Flow Boost for Employers

This measure will provide up to $25,000 back to business, with a minimum payment of $2,000 to eligible business that employ staff. The payment will be tax free.

However, it is worth noting that this is not a physical cash payment to small business, but a rebate of PAYGW that would ordinarily be payable to the ATO upon lodgement of a SMB BAS return (more info on this below).

To be eligible for this rebate, the business:

- Must have an aggregated annual turnover <$50 million, and

- Must employ workers

Key points include:

- The rebate will be delivered by the ATO as a credit to the business’ Integrated Client Account upon lodgement of activity statements, covering the period March – June 2020.

- Payment will be equal to 50% of the amount withheld from employee’s salary and wages, up to a maximum payment of $25,000.

- Eligible businesses that pay salary and wages will receive a minimum payment of $2,000 even if they are not required to withhold tax.

- Where this rebate places the business in a refund position, the ATO will deliver the refund within 14 days.

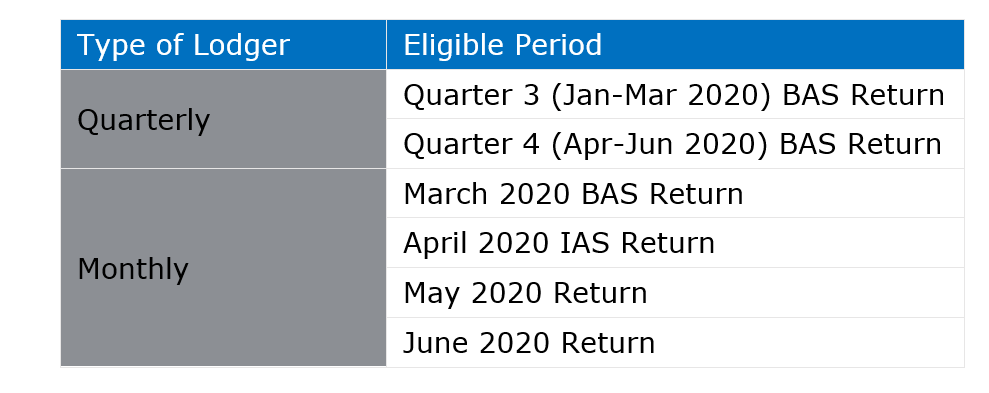

- Quarterly lodgers will be eligible to receive the payment for the quarters ending March 2020 and June 2020.

- Monthly lodgers will be eligible to receive the payment for the March 2020, April 2020, May 2020 and June 2020 lodgments.

- To provide a similar treatment to quarterly lodgers, the payment for monthly lodgers will be calculated at three times the rate (150 per cent) in the March 2020 activity statement.

- The minimum payment will be applied to the business’ first lodgment.

Those clients that are eligible to access this measure do not need to do anything as it will be dealt with automatically upon lodgement of activity statements.

It is worth noting that there is no great urgency for our clients to prepare and lodge the relevant activity statements. Our reasoning for this is that, unless the rebate will result in a refund (which will only occur if the rebate exceeds the net GST and PAYGI liability on the relevant return), the usual payment deadlines will still apply i.e. 25 May 2020 in respect of the March BAS return.

In our opinion, whilst it is a great initiative and will have a marked impact on our SMB clients, it doesn’t assist Sole Traders or Partnerships where salaries are not paid to the business owner/partners. Hence, they will lose out purely as a result of the structure that they chose to operate through.

Click here to access the Government’s Fact Sheet which includes a number of examples of how this rebate will be calculated.

2. Supporting Apprentices and Trainees

To support SMBs in retaining apprentices and trainees, eligible employers can apply for a wage subsidy of 50% of an apprentice or trainees wage paid during the 9 months from 1 Jan 2020 to 30 Sep 2020 – up to a maximum of $21,000.

To be eligible for this subsidy:

- Eligible to businesses employing fewer than 20 full-time employees who retain an apprentice or trainee

- The apprentice or trainee must have been in training with a small business as at 1 Mar 2020

Employers will be able to access the subsidy after an eligibility assessment is undertaken by an Australian Apprenticeship Support Network (AASN) provider.

Employers can register for the subsidy from early April 2020, and final claims for payment must be lodged by 31 Dec 2020.

3. Increasing the Instant Asset Write-Off

The Government is increasing the instant asset write-off threshold from $30,000 to $150,000 and expanding access to include all businesses with an aggregated turnover of less than $500 million (previously $50 million).

Key points to be aware of:

- The threshold applies on a per asset basis.

- Businesses can immediately write-off multiple assets.

- Applies from the date of the announcement (12 March 2020) until 30 Jun 2020, for new or second hand assets first used or installed ready for use in this timeframe.

As attractive as this measure might sound, we would not recommend rushing out the door to purchase that new vehicle you’ve always wanted. No doubt, the purchase of a new eligible asset will reduce your tax liability, or even mean you have no tax to pay at year-end.

However, more importantly are the cashflow implications and how this might negatively impact your business.

So, before you decide to purchase a new, expensive asset for the business, please contact your Mukiwa consultant to discuss whether this is the right approach for you.

4. Backing Business Investment

The Government is introducing a time limited 15 month (i.e. through to 30 June 2021) investment incentive to support business investment and economic growth, by accelerating depreciation deductions.

This investment incentive allows businesses with a turnover of less than $500m to accelerate depreciation deductions by providing an immediate deduction of 50% of the cost of eligible assets in the year of purchase (the balance to be depreciated using existing rules).

Eligible assets:

- Are new assets that can be depreciated under Division 40 of the Income Tax Assessment Act 1997, acquired after the announcement (12 March 2020) and first used or installed by 30 Jun 2020.

- Does not apply to second hand Division 40 assets, or buildings and other capital works depreciable under Division 43.

Again, we would recommend discussing this initiative with your Mukiwa consultant prior to the purchase of any assets.

5. Household Stimulus Package

Effective from 31 March 2020, $4.8 billion will be put aside to provide a one-off $750 tax-free stimulus payment to certain taxpayers (e.g. pensioners, social security and other income support recipients and eligible concession card holders).